Malaysia E invoice Compliance Review Framework:

Are You on Track for 2026?

- Published on

Since the phased implementation of mandatory e-Invoicing began in Malaysia on 1 August 2024, businesses across the country have been adapting to new digital tax requirements. As Malaysia approaches the final implementation phases in 2026, the national focus is shifting from system adoption to long-term compliance and enforcement.

To support this transition, the Inland Revenue Board of Malaysia (IRBM, also known as LHDNM or HASiL) introduced the E invoice Compliance Review Framework, which takes effect from 15 December 2025. This framework explains how IRBM will conduct compliance reviews to ensure businesses are meeting e-Invoicing requirements.

For businesses, this development is not a cause for alarm. Instead, it provides clarity. Understanding how the e-Invoicing Compliance Review Malaysia framework works allows companies to prepare early, strengthen internal processes, and operate with confidence as e-Invoicing becomes part of everyday business operations.

What Is the e invoice Compliance Review Framework in Malaysia?

The e-Invoicing Compliance Review Framework is an official guideline issued by IRBM that outlines the procedures its officers will follow when reviewing a taxpayer’s compliance with Malaysia’s e-Invoicing requirements.

Its purpose is to ensure that compliance reviews are conducted in a fair, transparent, and consistent manner. By clearly defining the review process, the framework helps businesses understand their rights, responsibilities, and what to expect during a review.

The framework officially comes into effect on 15 December 2025 and reflects IRBM’s broader approach of encouraging voluntary compliance while safeguarding the integrity of Malaysia’s digital tax system.

Why IRBM Introduced the e invoicing Compliance Review Framework?

The introduction of a formal compliance review framework is a natural next step in a nationwide digital initiative like e-Invoicing. IRBM has outlined several key reasons for this move:

- Strengthening Compliance and Transparency

A publicly defined review framework builds trust by ensuring e-Invoicing compliance checks are carried out fairly and consistently. - Ensuring Consistent Adoption Across Businesses

A standardised process allows IRBM to assess compliance uniformly across industries and business sizes, creating a level playing field. - Supporting Malaysia’s Digital Tax Ecosystem

The framework supports national priorities under Malaysia’s digitalisation agenda, including efforts outlined in the Twelfth Malaysia Plan (RMKe-12), by ensuring the secure and effective operation of digital tax infrastructure.

Key Components of Malaysia’s

e invoicing Compliance Review

Understanding the structure of the e invoice Compliance Review Malaysia framework helps businesses prepare effectively. The framework outlines several core components.

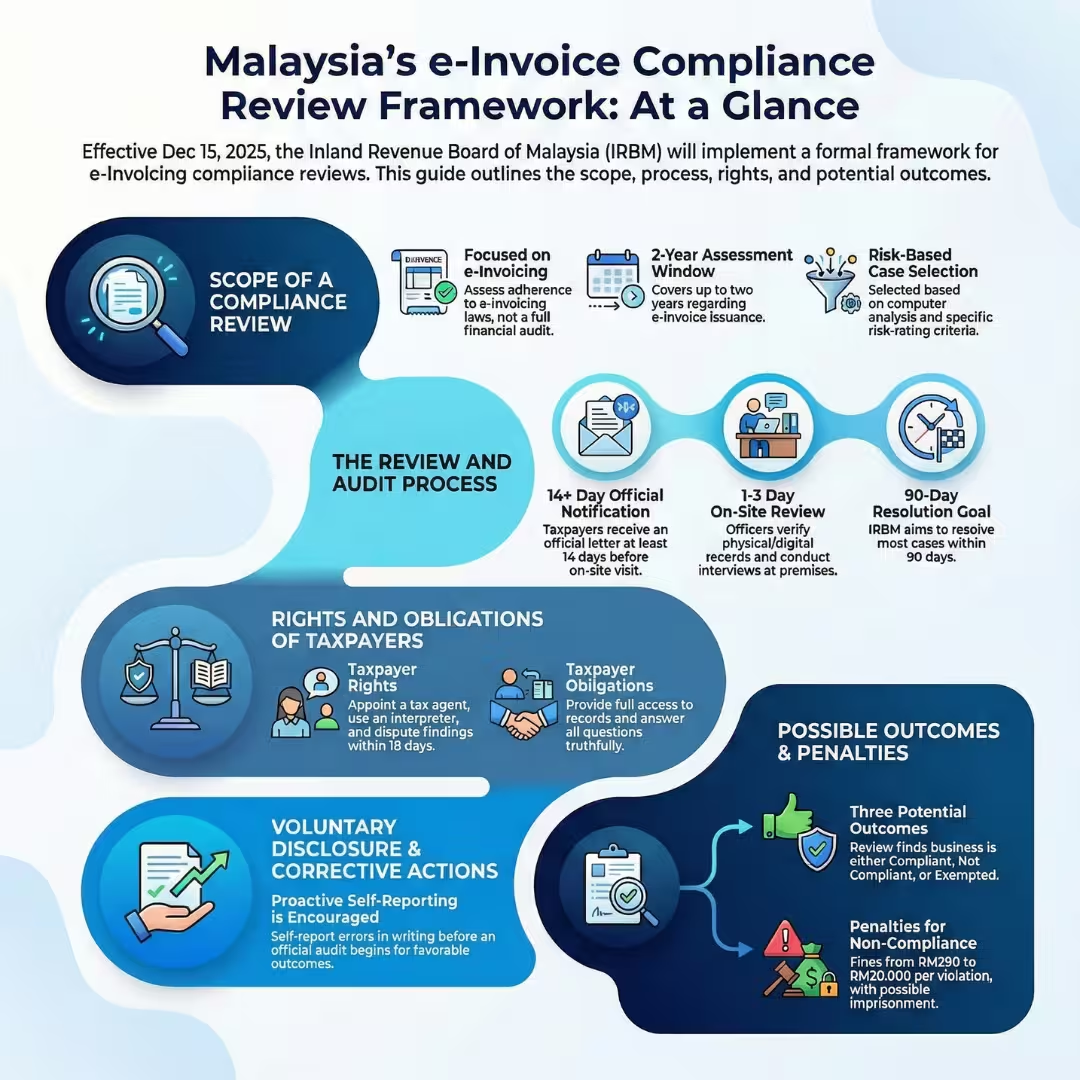

A. Scope of a Compliance Review

An e-Invoicing compliance review is not a full tax audit of a company’s finances. Instead, it focuses specifically on e-Invoicing obligations.

- Reviews assess adherence to laws and regulations governing the issuance and management of e-Invoices.

- A review may cover up to two (2) years of assessment.

- Case selection is based on risk assessment analysis, supported by information from various sources.

Because IRBM has access to transactional e-Invoice data, consistent and accurate invoicing from the outset is critical to reducing compliance risk.

B. The Review and Audit Process

If a business is selected for a review, IRBM follows a defined process:

- Notification

Businesses will receive a formal notice at least 14 calendar days before an on-site visit. - On-Site Review

Reviews typically last 1 to 3 days, depending on business complexity and cooperation. IRBM officers, known as e invoice Compliance Officers (PEI), are required to present official identification upon arrival. - Review Methodology

The review is conducted as a comprehensive review (semakan menyeluruh), involving interviews and examination of relevant records. These include sales and purchase invoices, debit and credit notes, refund documents, receipts, and electronic data stored within business systems.

C. Rights and Obligations of Taxpayers

The framework clearly outlines both taxpayer rights and responsibilities.

Taxpayer Rights

- The right to appoint a registered tax agent for representation.

- The right to request an interpreter if not fluent in Bahasa Melayu or English.

- The right to submit a formal objection within 18 calendar days if findings are disputed.

Taxpayer Obligations

- Full cooperation with IRBM officers during the review.

- Providing access to premises, records (physical and electronic), and reasonable facilities.

- Answering all questions truthfully and accurately.

D. Voluntary Disclosure and Corrective Actions

IRBM encourages businesses to be proactive. Taxpayers may submit a voluntary disclosure in writing if they identify errors or non-compliance before a review is initiated.

This provision signals IRBM’s preference for early correction over enforcement. For businesses, addressing issues promptly demonstrates good faith and may lead to more favourable outcomes.

E. Possible Outcomes of Non-Compliance

A compliance review may result in one of three findings:

- Compliant

- Not Compliant

- Exempted

For cases of non-compliance, penalties may be imposed under Section 120(1)(d) of the Income Tax Act 1967, including fines ranging from RM200 to RM20,000, imprisonment, or both. These penalties may apply per instance of non-compliance, making accuracy essential.

Who Should Pay Attention to This Framework?

The e-Invoicing Compliance Review Malaysia framework applies to all businesses required to issue e-Invoices, including:

- MSMEs and growing businesses, especially those preparing for mandatory phases in 2026.

- Business owners and finance teams responsible for daily compliance.

- Accountants and tax professionals managing client e-Invoicing obligations.

What does the e invoice Compliance Review Means for Businesses in 2026

As enforcement becomes more structured, businesses should expect several operational implications:

- Higher Expectations for Accuracy

From 2026 onwards, all transactions — including sales, purchases, returns, and adjustments — must be accurately captured and submitted in real time. - Structured Record-Keeping Is Essential

IRBM officers are authorised to review both physical and electronic records. Organised, accessible digital records are no longer optional but fundamental to compliance. - Manual Processes Increase Risk

Manual invoicing and disconnected spreadsheets increase the likelihood of inconsistencies. Fragmented data can complicate reviews and raise compliance concerns. - A Shift Toward Operational Discipline

While earlier phases focused on implementation, 2026 onwards emphasises consistent, day-to-day accuracy. E-Invoicing becomes an ongoing operational standard rather than a one-time setup.

How Businesses Can Prepare for an e invoice Compliance

Proactive preparation remains the most effective strategy. Businesses can take the following steps:

- Maintain Accurate and Consistent Records

Ensure all transactions are properly recorded, including relevant e-Invoice data and timestamps. - Review Your Invoicing Workflow

Map your invoicing process end to end and conduct internal checks to ensure every document aligns with IRBM guidelines. - Adopt a Compliant Digital Accounting Solution

Modern cloud-based platforms, such as N3 AI Accounting (formerly QNE AI Cloud Accounting), are designed to support IRBM e-Invoicing requirements by improving data accuracy, maintaining structured records, and streamlining compliance workflows — helping businesses prepare confidently for compliance reviews.

Preparing for Malaysia’s e-invoicing Future with Confidence

The e-Invoicing Compliance Review Framework is a natural and expected part of Malaysia’s transition to a digital-first tax system. By providing transparency and structure, it enables businesses to understand expectations and prepare with clarity.

Rather than viewing compliance reviews as a risk, businesses can treat them as an opportunity to strengthen financial discipline and improve operational efficiency. With the right processes and reliable digital tools in place, navigating Malaysia’s e-Invoicing requirements becomes significantly easier.

As e-Invoicing becomes embedded in daily business operations, proactive preparation today will ensure smoother compliance tomorrow, allowing businesses to move forward with confidence.

Frequently Asked Questions (FAQs)

What are the main requirements for e invoice compliance in Malaysia?

Businesses must issue and manage all e-Invoices according to IRBM regulations, ensuring accurate, real-time recording of sales, purchases, returns, and adjustments. Maintaining structured digital records and aligning invoicing workflows with the framework is essential for compliance.

This one-year interim relaxation is intended to help Phase 4 businesses, particularly MSMEs, adjust their systems and workflows. However, IRB has clarified that this does not exempt businesses from implementing e-invoicing during 2026; it only suspends penalties while implementation is in progress.

What are the penalties for non-compliance with e-invoice regulations in Malaysia?

Phase 4 businesses should review their invoicing processes against the IRB’s e-Invoice Specific Guidelines, including requirements for consolidated invoices, self-billing scenarios, transaction descriptions, and buyer requests for individual e-invoices.

Conducting a gap analysis of the order-to-cash cycle—from sales to invoicing and record-keeping—helps identify what changes are needed before full enforcement resumes after 31 December 2026. Using a cloud-based accounting system with built-in e-invoicing can simplify this assessment, as many compliance checks are system-driven.

Which software solutions support Malaysian e invoice compliance standards?

Cloud-based accounting platforms like N3 AI Accounting (formerly QNE AI Cloud Accounting) are designed to meet IRBM e-Invoicing requirements. They help businesses automate workflows, maintain structured records, capture accurate data, and prepare for compliance reviews efficiently.

How can businesses prepare for an e-invoicing compliance review in Malaysia?

Businesses should maintain accurate records, review invoicing workflows, and adopt compliant digital accounting solutions. Ensure access to electronic and physical records and proactively disclose any errors to IRBM to demonstrate good faith.

How do cloud-based e invoice compliance tools work in Malaysia?

Cloud-based e invoice compliance tools in Malaysia help businesses create, manage, and maintain e-Invoices in line with IRBM requirements. They automate record-keeping, reduce manual errors, and make invoice data easier to retrieve during a Compliance Review Framework (CRF) audit.